What Makes a Long Island Waterfront Listing Worth the Premium — And How to Tell If It Is

Waterfront listings on Long Island routinely sell for two, three, sometimes four times the price of a comparable inland home a quarter mile away. The premium is real and the demand is durable. But “waterfront” is one of the loosest words in residential real estate — a category that covers everything from a true deep-water deeded parcel with a working dock to a house with a partial view of the Sound across a public road and a neighbor’s hedge. The difference at the closing table can be several hundred thousand dollars.

When I’m walking a waterfront listing with a buyer, the first thing I do is stop calling it waterfront in my head until I’ve checked four things: how the property actually touches the water, what the seller is allowed to do at the shoreline, what FEMA says about the parcel, and what the bulkhead or structure separating the house from the water is hiding. None of that shows up in the listing photographs. Most of it doesn’t even show up in the listing description. All of it should show up before you sign a contract.

The Difference Between ‘Water View’ and True Waterfront Access

The listing language matters. “Waterfront” implies direct frontage on a navigable body of water with the legal right to access it from your own parcel. “Water view” means the house can see water from one or more windows — sometimes spectacularly, sometimes from the second-floor bathroom on a clear day in February. “Beach community” or “water access” usually means a shared association easement to a community beach or a launch, which is its own thing and can be lovely, but it is not the same financial asset.

The distinction is not pedantic. A true waterfront parcel on Long Island Sound or in one of the protected North Shore harbors carries a defensible premium because the asset is scarce and reproduces poorly — there is a finite number of feet of shoreline in Suffolk County and most of them are already accounted for. A water-view parcel two lots back from the water, in a saturated submarket with comparable inland inventory, is competing on a different curve.

Before I take a buyer’s offer seriously on a waterfront listing, I want the survey in front of me. Specifically: I want to see where the mean high water line sits relative to the surveyed property line. On Long Island Sound and the bays, that’s often a contested boundary, especially on bluff properties where erosion has shifted the natural line over decades. The survey is the document that tells you what you’re buying. The listing description is the document that tells you how the seller wants you to feel about what you’re buying.

How Bulkhead Condition, Dock Rights, and Riparian Rights Affect Value

Three different categories of right or structure, all routinely lumped together in conversation, all wildly different in their financial and legal weight.

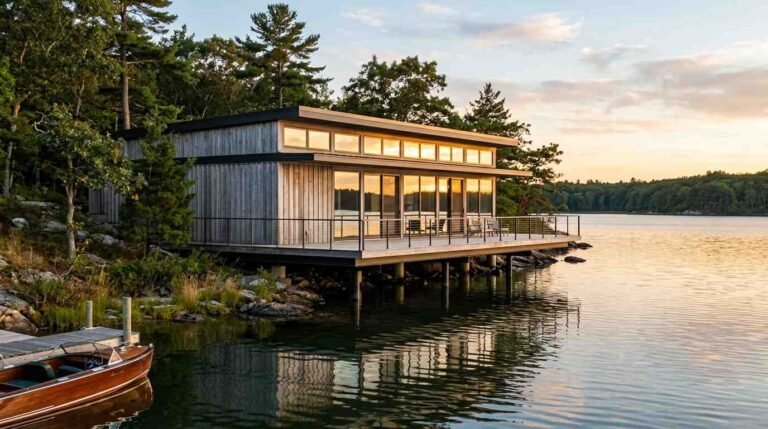

Bulkheads are the engineered walls — usually steel, treated timber, vinyl sheet, or stone — that hold the upland in place against tidal action and storm surge. On the North Shore, where bluff properties drop sharply to the water, a failing bulkhead is the single most consequential thing a waterfront buyer can inherit. Replacement runs into six figures routinely and seven on larger frontages, and the New York State Department of Environmental Conservation regulates the permit pathway closely. If the listing photos are flattering and the bulkhead is twenty-five years old and undocumented, that’s not a discount — that’s a budget line you have not yet drawn.

Dock rights are not the same as the right to use a dock. A property may have a structure called a dock that was built decades ago under a permit that has since lapsed, expired, or was never properly transferred at sale. Whether you can use it, repair it, replace it, or extend it is a function of state, town, and sometimes federal jurisdiction. The U.S. Army Corps of Engineers, the New York State DEC, and the local town all have a say. A Connecticut waterfront broker put this well in a recent buyer’s guide on the lower Connecticut River, noting that buyers should request copies of state or federal permits and confirm no pending actions affect navigation or moorings. The same logic applies on every Sound-facing parcel in Suffolk County.

Riparian rights — or more accurately on Long Island Sound, littoral rights, which apply to tidal and standing water — are the underlying legal entitlements of an upland owner to access and reasonable use of the adjacent waterbody. They are valuable and they are not absolute. They are constrained by public trust doctrine, by state-owned submerged lands, and by recorded easements that may or may not appear cleanly in a title commitment. I tell buyers to budget the same level of attorney review for a waterfront deal that they’d budget for a multi-parcel commercial transaction. The complexity rewards it.

There is a separate piece I’ve written on dock rights and mooring rights for North Shore waterfront buyers that goes deeper into the distinction — worth reading in tandem with this one.

Flood Zone Designation: What It Costs You Beyond the Purchase Price

Every waterfront listing on Long Island sits inside a FEMA flood zone of some designation. The question is which one. AE, VE, X (shaded), X (unshaded) — these are not abstract codes. They translate directly into insurance premiums, lender requirements, building restrictions, and, in the long run, resale exposure.

A property in a VE zone — the high-risk Velocity zone, meaning subject to wave action during a base flood — will carry meaningfully higher National Flood Insurance Program premiums than the same house ten feet of elevation away in an AE or X zone. Lender requirements may also restrict what kind of mortgage product is available. And the FEMA maps themselves are being updated more aggressively than they have been in decades — the parcel that was barely outside the special flood hazard area in 2015 may not be in 2026.

I’ve written about the FEMA map issue specifically for Sound-facing properties in Flood Insurance on Long Island’s North Shore. The short version: if you’re buying waterfront, get an Elevation Certificate before you finalize the offer, not after the inspection contingency expires. The certificate is the single most predictive document for what your annual insurance cost will look like over the next decade.

North Shore vs. South Shore Waterfront — Which Holds Value Better?

Different geographies, different value profiles, and I want to be careful here to describe rather than rank — both shores have premium markets and both have softer pockets, and a comparison done at the wrong scale is misleading.

North Shore waterfront — Long Island Sound, the protected harbors from Cold Spring Harbor east to Mount Sinai Harbor and the deeper water at Port Jefferson — tends to feature higher elevations, bluff conditions, and properties where the structural relationship to the water is more architectural than recreational. The boating culture is real but constrained by the depth and tidal range. The historical and architectural inventory skews older and more significant — Gold Coast estates, mid-century cliff houses, restored colonials.

South Shore waterfront — Great South Bay, the inlets, the barrier beach communities — features lower elevations, more direct boating access, more bayfront and canal properties, and a higher density of true recreational waterfront. The flood exposure profile is also different, with more parcels in VE zones and a more aggressive sea-level adjustment trajectory.

Which holds value better depends entirely on what the buyer is buying. A North Shore harbor parcel with a working dock and a pre-Civil War main house holds value on a different curve than a Great South Bay canal house with a new lift and direct ocean access through Fire Island Inlet. Both can be excellent. Neither is automatically the better investment.

What I tell buyers: the question isn’t North Shore versus South Shore. The question is whether the specific parcel has the structural fundamentals — bulkhead, elevation, access, rights — that will let it survive the next thirty years of weather and regulation without becoming a liability. That answer doesn’t depend on which shore. It depends on the file.

Red Flags Buyers Miss on Waterfront Listings

A short list of things I check on every waterfront walkthrough that buyers often miss in the photographs:

The first is the bulkhead toe — the bottom edge, at the water. Voids, scour, sagging, or fresh emergency patching at the toe are the visible signs of structural failure that the upland landscaping is hiding. A bulkhead can look fine from the lawn and be six months from failure at the water.

The second is the dock electrical service. If there’s shore power, I want to see a recent inspection. Older dock wiring is a serious fire and shock hazard, especially in salt environments, and the cost of bringing it to current code is non-trivial.

The third is the mooring or slip arrangement. If the property advertises mooring privileges, the question is whether those privileges transfer with the deed or are issued seasonally by the town or harbor master. Many North Shore harbors operate on annual permit cycles that do not automatically transfer at sale.

The fourth is the oil tank. North Shore older inventory frequently includes buried oil tanks — sometimes documented, sometimes not. A buried tank near a waterfront parcel is a different conversation than one inland because remediation triggers DEC scrutiny and potentially Sound water quality reporting. I’ve written separately about the oil tank discovery protocol mid-renovation — relevant here.

The fifth — and this is the one that costs people the most — is the surrounding parcel pattern. A waterfront parcel that sits next to a public access easement, a town launch, or a planned shoreline restoration project will not appreciate the same way as one in a fully residential cluster. The neighbors and the public infrastructure are part of the asset. They show up at closing whether or not anyone names them.

Pawli’s take: I’d rather see a buyer walk away from a waterfront listing that doesn’t pass scrutiny than win the bidding war. The premium on the right waterfront parcel is real and the appreciation curve is durable. The premium on the wrong one is a long expensive education in coastal engineering, regulatory law, and the actuarial mathematics of climate exposure. The difference is almost always knowable before the contract. It just takes the right questions, asked in the right order, before anyone falls in love with the view.

You Might Also Like

- Dock Rights, Mooring Rights, and the Difference: What North Shore Waterfront Buyers Need to Settle Before Closing

- Flood Insurance on Long Island’s North Shore: What FEMA Maps Don’t Tell You About Sound-Facing Properties

- Sound vs. Bay vs. Harbor: What the Water Type Actually Means for Your Maintenance Budget and Resale Value

- Holding Back the Sound: The Brutal Economics of North Shore Bulkheads

- How to Read a Waterfront Lot Survey Before You Make an Offer

Real estate markets change. This post reflects market conditions as of May 2026. For current listings and waterfront market data, contact Pawli at Maison Pawli. This post is for informational purposes only and is not legal or financial advice — consult a licensed attorney and financial advisor for your specific situation.

Sources

- New York State Department of Environmental Conservation — Tidal Wetlands Permits

- FEMA Flood Map Service Center

- U.S. Army Corps of Engineers — New York District Regulatory Program

- National Flood Insurance Program — FEMA

- Teri Lewis Real Estate — Buying on the River in Essex Village: Key Details to Know (March 2026)

- New York State Department of State — Coastal Resources