What Commercial Sellers on Long Island Get Wrong About Timing, Tenants, and the Transfer of Leases

Last spring, I toured a small retail strip in Miller Place — four units, fully occupied, decent visibility from Route 25A. The owner had listed it at a cap rate he’d calculated himself, using rents that were current but leases that weren’t. Two of his four tenants were on month-to-month arrangements that had rolled over from term leases years earlier. One was paying below-market rent established in 2019 and hadn’t been adjusted since. The listing sat for seven months.

The building wasn’t the problem. The lease structure was.

Commercial real estate on Long Island gets a fraction of the attention in seller strategy conversations that residential does — understandably, because the volume of commercial transactions is smaller and the universe of sellers is more specialized. But the mistakes commercial sellers make are, in my experience, both more consequential and more correctable than the ones residential sellers make. And with Long Island’s commercial market showing the kind of bifurcation it’s showing right now — retail and industrial performing, office struggling — the gap between a well-prepared commercial listing and a poorly prepared one is wider than it’s been in years.

Here are the three things Long Island commercial sellers most consistently get wrong.

1. Timing Against the Tenant Cycle, Not the Market Calendar

Residential sellers are trained to think about seasonality — spring is busy, January is slow. Commercial buyers don’t operate on a seasonal rhythm. They operate on a tenant cycle.

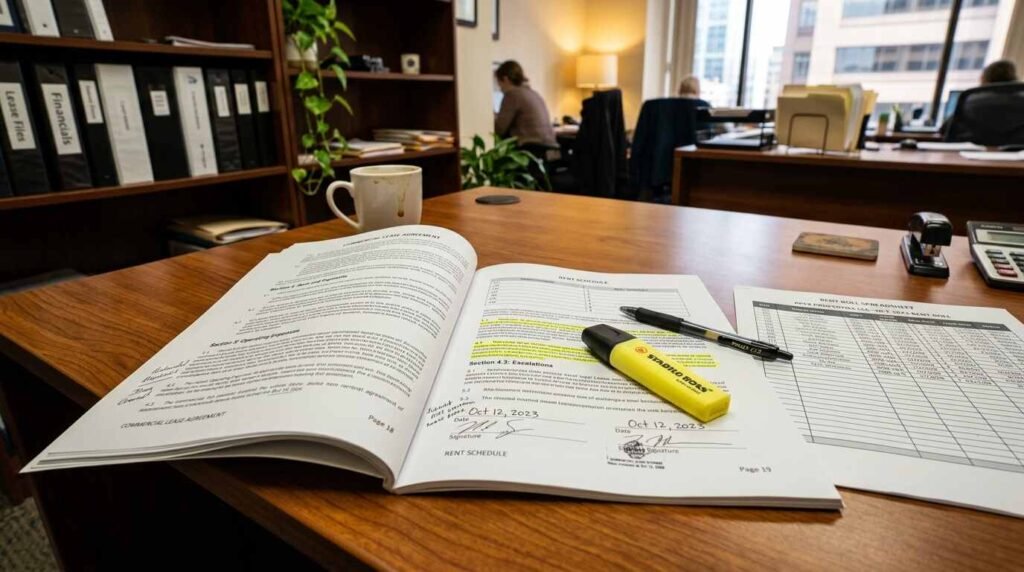

The most valuable commercial building is one where a buyer can project stable, long-term income from day one. That means tenants on active, enforceable leases with meaningful remaining terms and clearly defined renewal options. When a commercial seller lists at a moment when their tenant leases are stale, expired, or month-to-month, they’re not just giving a buyer something to negotiate on — they’re fundamentally changing the risk profile of the asset.

Long Island’s retail market is seeing rapid backfilling of second-generation spaces by food and beverage, medical, and experiential tenants, with overall vacancy expected to remain stable below national averages. That’s a healthy demand environment — but it doesn’t help a seller whose tenants are all month-to-month. A sophisticated buyer looking at a fully occupied Long Island retail strip with four month-to-month tenants isn’t buying a fully occupied building. They’re buying four tenants who could leave or renegotiate the moment the sale closes. The cap rate calculation reflects that.

The strategic move — and it’s one most sellers don’t make, because it requires thinking about the sale eighteen to twenty-four months out — is to negotiate lease renewals with your existing tenants before you list. Bring the leases to term. Get signed documents. Let the building age a year with renewed paper in place before you go to market. The difference in perceived value — and in actual negotiation leverage — is substantial.

2. Underestimating What Buyers Actually Pay Attention to in a Lease

Most commercial sellers think buyers care about the rent number. Buyers care about the rent number last.

What sophisticated commercial buyers look at first: lease expiration dates, renewal option language, rent escalation provisions, assignment and subletting clauses, landlord repair obligations, and — critically — what happens to those leases when ownership transfers.

The assignment clause is where a lot of Long Island commercial deals get complicated at the contract stage. A commercial lease may require tenant consent to an ownership transfer. If your tenant has the contractual right to withhold consent or to exercise a right of first refusal on the sale, that’s a material variable that a buyer needs to know about before they spend money on due diligence. Sellers who disclose this early, who have already had the conversation with their tenants and documented the outcome, are in a dramatically stronger position than sellers who let buyers discover it during the due diligence period.

I’m not providing legal advice here — and on commercial lease transfer mechanics, you want a New York commercial real estate attorney, not general guidance. But I will say that the sellers who walk into a commercial listing having had their attorney review every lease for assignment provisions, change-of-control clauses, and tenant consent requirements are the sellers who close cleanly. The ones who hand over the lease abstracts and hope for the best are the ones who end up renegotiating price after the buyer’s attorney has reviewed the documents.

3. Misreading How Buyers Underwrite the Asset

Here is where the disconnect between residential and commercial seller thinking is most stark.

A residential buyer thinks: I love this kitchen. A commercial buyer thinks: at this price, what yield am I generating on my equity, and how does that compare to what I could get elsewhere?

Commercial buyers — certainly the serious ones, the ones who will actually close — are underwriting cap rates, debt service coverage ratios, and total return projections. They are comparing your building to other opportunities in the same risk tier. If your asking price implies a 5.5% cap rate but comparable stabilized retail assets in Suffolk County are trading at 6.2%, you will either need to justify the premium or adjust the price. There is no emotional ask that closes that gap.

Adaptive reuse has moved from opportunistic to strategic — across office, retail, and institutional real estate, owners are increasingly evaluating whether existing assets can be repositioned rather than replaced. For Long Island commercial sellers, this matters because buyers are now often underwriting not just the current use but the conversion potential. A dated strip center in a high-visibility corridor isn’t just a retail investment anymore — it’s potentially a medical office conversion, a mixed-use redevelopment parcel, or a last-mile logistics site, depending on the zoning. Sellers who understand and can articulate what a buyer could do with the land and the structure — not just what they’re currently doing with it — position their property as a more complex opportunity, which tends to attract more sophisticated buyers and more competitive pricing.

I wrote about this in a broader architectural context when I covered how Long Island’s obsolete retail strip centers are being reconsidered as structural raw material. The valuation conversation for commercial sellers has the same underlying logic: what is this building worth as it sits, and what is it worth to someone who sees what it could become?

The Long Island Commercial Market in 2026

Worth stating plainly: this is not a uniform market. Long Island’s office market is characterized by a price-performance paradox, where asking rents have reached five-year highs despite persistent negative net absorption — the overall office vacancy rate recently climbed to 11.4%. If you’re selling an office building or an office condo on Long Island, the buyer pool is narrower, the underwriting is more conservative, and the timeline to close is longer than it was five years ago.

Retail and industrial are different stories. Industrial fundamentals remain some of the tightest in the Northeast, with rising rents and healthy development activity. Well-located retail with strong tenants continues to perform. The error commercial sellers make is assuming their experience of the market — based on what their cousin got for a building in Melville in 2019 — translates to their asset type and location in 2026. It may not.

What a Well-Prepared Commercial Listing Looks Like

In my view, a commercial seller who is genuinely prepared to go to market has done the following before listing:

Had every lease reviewed by a commercial real estate attorney for assignment provisions, renewal rights, and transfer mechanics. Resolved the month-to-month situations — either by getting signed renewals or by disclosing clearly that those tenants are rolling and pricing that risk into the ask. Pulled a current rent roll with actual lease expiration dates, not estimates. Run a basic cap rate analysis using the actual Net Operating Income — not the gross rent — and compared it to recent comparable sales in the submarket. Had a conversation with any tenant who has a right of first refusal or a consent-to-sale provision.

None of this is complicated. All of it takes time. The sellers who do it before listing spend that time once, in advance, from a position of control. The sellers who don’t do it spend far more time mid-contract, under deadline pressure, fixing the things buyers have found.

The mechanics aren’t different from what I wrote about residential sellers and the pre-listing inspection. The principle is identical: the information is going to surface. The only question is whether you surface it on your terms or on the buyer’s.

This is for informational purposes only — consult a licensed real estate attorney and financial advisor for guidance specific to your commercial transaction.

Real estate markets change. For current listings and market data, contact Pawli at Maison Pawli.

Sources

- TenantBase — Long Island Commercial Real Estate Market Report Q1 2026: https://www.tenantbase.com/long-island/q1-2026/

- Van Vlissingen & Co. — 6 Commercial Real Estate Trends in 2026: https://www.vvco.com/6-commercial-real-estate-trends-in-2026/amp/

- First Class Management — NYC Commercial Real Estate Market Outlook 2026: https://www.fcmre.com/nyc-commercial-real-estate-market-outlook-what-to-expect-in-2026/

- Forchelli Deegan Terrana Law (Mineola, NY) — Commercial Lease and Real Property resources: https://www.forchellilaw.com/

- New York State Bar Association — Commercial Real Estate Committee resources: https://nysba.org/sections/real-property-law/