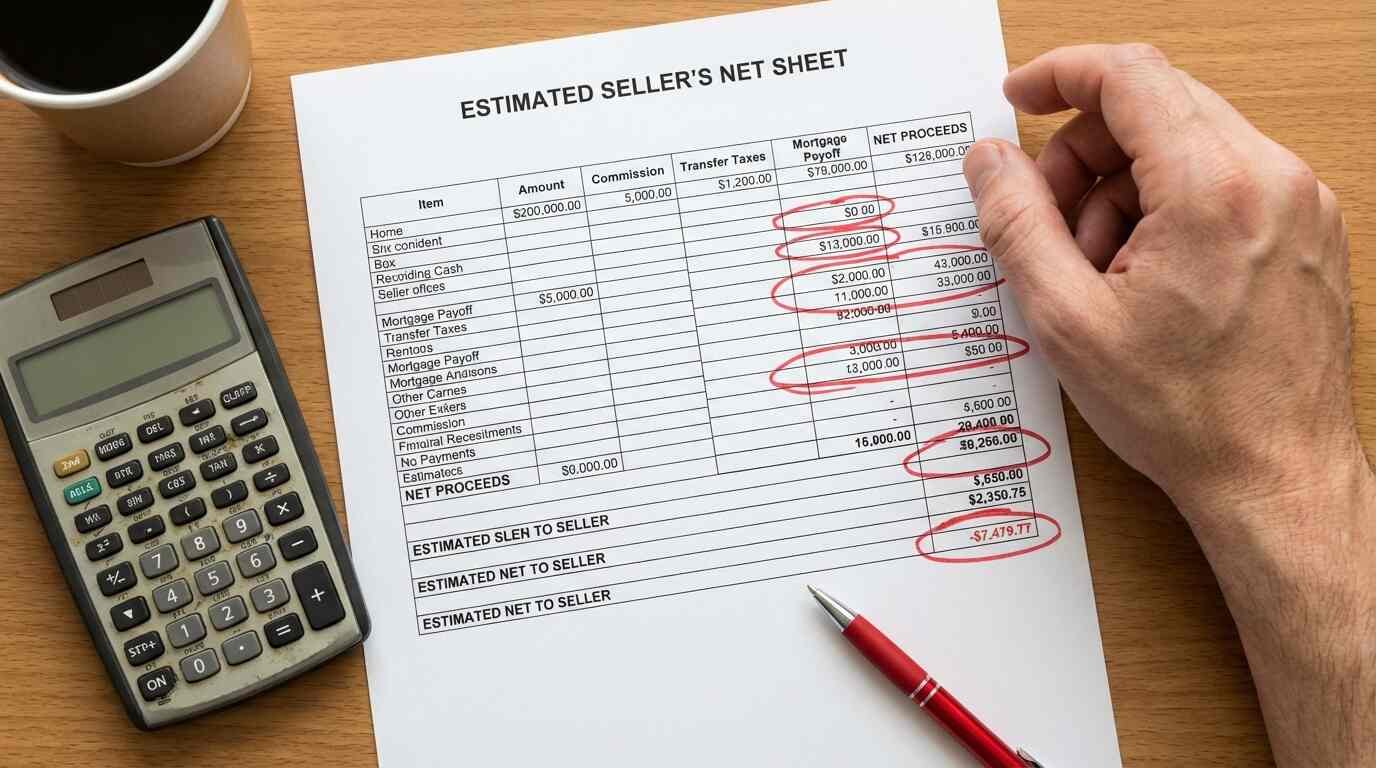

The Seller Net Sheet Is Not a Legal Document — and That Omission Has Consequences

Before a property lists, the seller receives a document that projects their proceeds from the sale — estimated sale price, agent commissions, title fees, transfer taxes, outstanding mortgage payoff, and a net number that represents what they’ll take home from closing. This document is the seller net sheet. It is the financial foundation on which sellers make one of the largest decisions of their lives.

It is not a legal document. It carries no regulatory weight. And when it is wrong — materially, consequentially wrong — the seller’s remedies are limited in ways that most sellers don’t discover until after the damage is done.

What the Net Sheet Is

The seller net sheet is an estimate, prepared by the listing agent, of the seller’s projected proceeds based on a set of assumptions: the anticipated sale price, the commission rate, the applicable transfer taxes, and the estimated payoff of any outstanding mortgage as of the anticipated closing date. In some cases it includes estimated closing credits, attorney fees, and inspection or repair allowances.

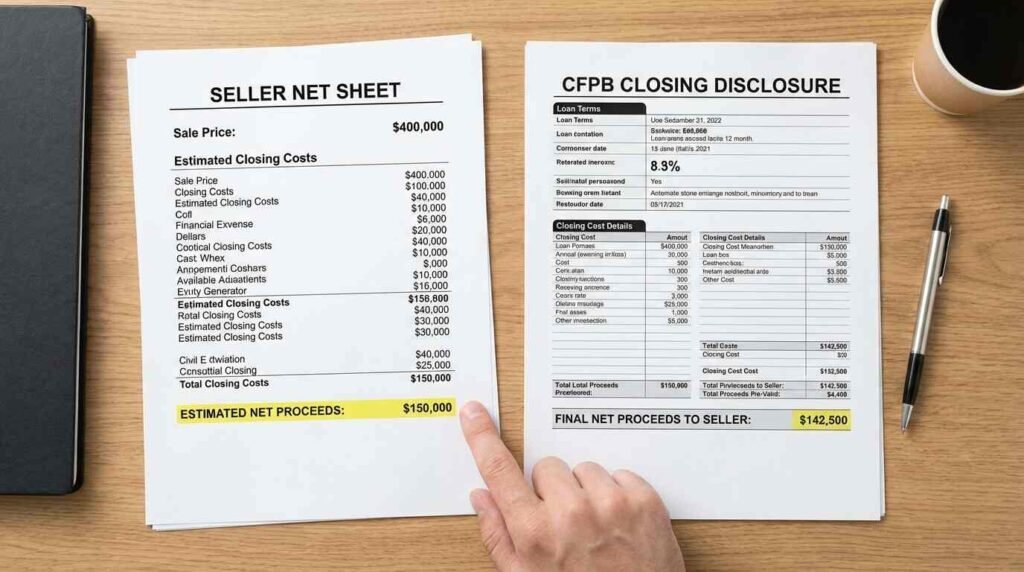

The CFPB’s Closing Disclosure form — required under TRID (TILA-RESPA Integrated Disclosure) for purchase transactions involving financing — is the legally binding document that governs the actual financial terms of closing. It is prepared by the lender or closing agent, reviewed by all parties, and subject to specific regulatory requirements as to accuracy and delivery timing under 12 C.F.R. § 1026.19. Errors on the Closing Disclosure are subject to regulatory correction requirements.

The seller net sheet is none of these things. It is prepared by the listing agent, is subject to no regulatory format requirements, is not reviewed by the lender, and carries no statutory obligation of accuracy beyond the general duty of honest dealing.

The Regulatory Gap

California Business and Professions Code § 10176(a) provides the statutory basis for agent discipline for misrepresentation in real estate transactions — including written representations about financial terms. Ohio Administrative Code § 1301:5-1-02 contains parallel provisions. Every state has some version of this statute. What none of them do is specifically regulate the format, methodology, or accuracy standards of the seller net sheet.

NAR Code of Ethics Articles 1 and 12 require Realtors to deal honestly with clients and the public and to avoid misrepresentation. An agent who knowingly provides a materially inaccurate net sheet has violated these provisions and is subject to professional discipline. But the Code of Ethics is not a statute, and its enforcement is through arbitration panels and professional associations — not courts.

The practical result is that sellers who rely on a materially inaccurate net sheet and suffer financial harm have claims that sound in fraud or misrepresentation but face the evidentiary burden of proving the agent’s intent or knowledge — because negligent inaccuracy, without more, is typically insufficient for a fraud claim.

Where Net Sheets Go Wrong

In my experience, the net sheet errors that cause real harm cluster in a few categories.

Mortgage payoff miscalculation. The payoff amount on a mortgage changes daily as interest accrues. An agent who calls for a payoff quote but uses a figure from 45 days before the closing date — or who estimates the payoff rather than requesting the official figure — can produce a net sheet that overstates the seller’s proceeds by thousands of dollars. Official payoff quotes from the lender are the only reliable source, and they must be current.

Transfer tax understatement. New York’s combined real property transfer taxes — the state transfer tax, the mansion tax where applicable, and the New York City real property transfer tax for properties in the city — are specific statutory calculations applied to the purchase price. An agent who rounds, estimates, or applies the wrong rate produces a net that doesn’t reflect actual closing costs. On a $1.2 million sale subject to the mansion tax, the error can be material.

Commission arithmetic. Net sheets prepared before a buyer is identified sometimes reflect commission structures that change during negotiation — particularly where the buyer’s agent commission is contested or where the seller has negotiated a modified rate. If the net sheet reflects a commission rate that doesn’t match the eventual transaction, the net is wrong.

Repair credit omissions. When inspection negotiations result in a seller credit, the net sheet should be updated to reflect it. Sellers who receive a pre-listing net sheet and don’t receive an updated version after credits are negotiated are working from a number that no longer reflects the transaction.

What Sellers Should Demand

Before listing, sellers should ask their agent for the basis of each line item on the net sheet — not just the number. The mortgage payoff should come from a lender-issued payoff statement, not an estimate. The transfer taxes should be calculated using the current statutory rate applied to the anticipated sale price. The commission should reflect the listing agreement’s precise language.

After an accepted offer, the net sheet should be updated to reflect actual contract terms, including any inspection credits, closing date adjustments that affect the mortgage payoff, and any seller-paid buyer agent compensation. The updated net sheet should be compared to the Closing Disclosure when it is received — typically three business days before closing — and any discrepancies investigated before the closing date.

The Closing Disclosure is the legal document. The seller net sheet is the projection. A seller who understands that distinction — and who manages the gap between them actively — is a seller who arrives at the closing table without surprises.

This post is for informational purposes only and does not constitute legal or financial advice. Consult a licensed real estate attorney and financial advisor regarding the specific terms and financial projections for your transaction.

Sources:

- TRID Rule, 12 C.F.R. § 1026.19: https://www.consumerfinance.gov/rules-policy/final-rules/tila-respa-integrated-disclosure-rule/

- CFPB Closing Disclosure: https://www.consumerfinance.gov/owning-a-home/closing-disclosure/

- California Business and Professions Code § 10176: https://leginfo.legislature.ca.gov

- Ohio Administrative Code § 1301:5-1-02: https://codes.ohio.gov

- NAR Code of Ethics, Articles 1 and 12: https://www.nar.realtor/about-nar/governing-documents/code-of-ethics

You Might Also Like: For a complete overview of everything involved in selling on the North Shore — pricing, staging, legal obligations, and closing — see The North Shore Seller’s Guide.