New Suffolk County Flood Zone Remapping Is Here — What It Means for Your Homeowner’s Insurance

There is a letter some Long Island homeowners receive and immediately set aside. It comes from their insurance company, or sometimes directly from their lender. It references FEMA, it references flood zones, and it uses an acronym — FIRM — that most people have never looked up. Then comes the line they actually notice: their annual insurance cost is going up, sometimes by thousands of dollars. Or, occasionally, going down — but that never seems to get the same attention.

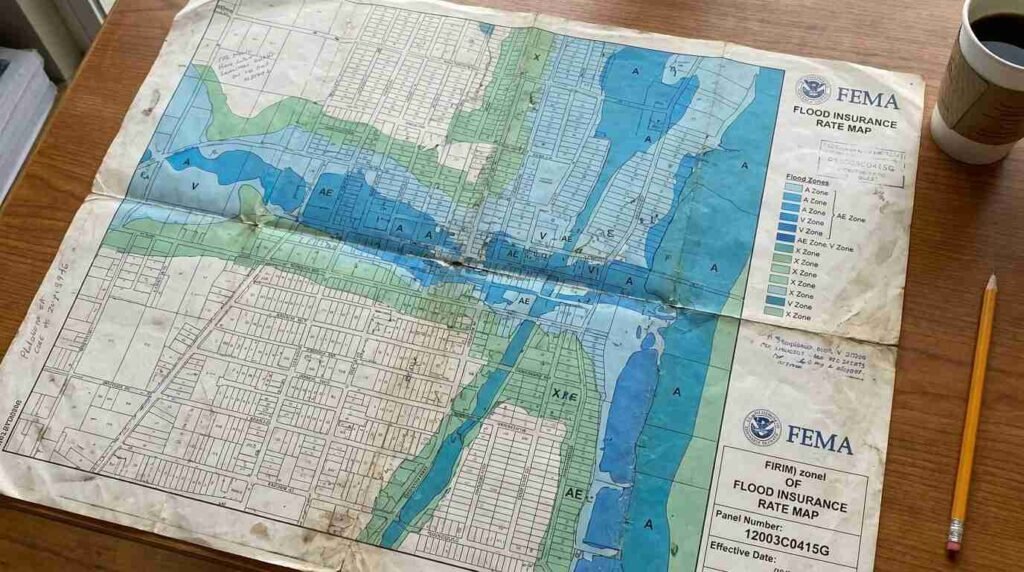

Flood Insurance Rate Maps, the FIRMs that FEMA maintains and periodically updates, are the documents that determine whether a property sits in a high-risk flood zone, a moderate-risk zone, or minimal-risk territory. For homeowners with federally-backed mortgages in high-risk zones, flood insurance isn’t optional — it’s a lender requirement. A zone change can make the difference between a $400-a-year policy and a $4,000-a-year obligation, or it can eliminate a mandatory coverage requirement entirely, freeing up real purchasing power in a buyer’s monthly budget.

This is a story I track closely, because flood zone designation touches nearly every coastal and near-coastal transaction I handle on the North Shore.

Which Suffolk County Towns Are Affected by the New Flood Maps

Suffolk County’s coastline — spanning Long Island Sound on the north shore, Great South Bay and Atlantic-facing beaches on the south, the Peconic Bay system on the east — gives it among the most varied and complex flood mapping profiles of any county in New York State. FEMA maps for Long Island have not been comprehensively updated since the years following Superstorm Sandy in 2012, when preliminary revised maps drew significant pushback from municipalities and homeowners alike.

FEMA’s National Flood Insurance Program operates on a rolling update cycle. Letters of Map Amendment (LOMAs) and Letters of Map Revision (LOMRs) are issued continuously as individual property owners or municipalities challenge their designations with hydrological data. The broader map update process — which involves new coastal flood studies, updated storm surge modeling, and coordination with local floodplain managers — moves on a longer cycle.

For buyers and sellers in Suffolk County, the practical question is always: what map is currently in effect for this property, and is there an active revision in process? The FEMA Map Service Center at msc.fema.gov allows any homeowner to enter an address and see the current FIRM panel that applies to their property, including effective dates. This is the starting point for any flood zone due diligence on a transaction.

Coastal communities with the highest concentration of designated flood zones in Suffolk County include communities along the Sound-facing bluffs and coves of the North Shore — Mount Sinai Harbor, Port Jefferson Harbor, Setauket Harbor, Centerport Harbor — as well as barrier beach communities on the South Shore and the creek-adjacent lots throughout the Peconic watershed.

How a Zone Change Can Spike — or Reduce — Your Insurance Premium

FEMA designates flood zones using letter codes that determine both risk level and insurance requirements. The key designations for residential buyers:

Zone X (or Zone C on older maps) — minimal to moderate flood risk. Flood insurance is not federally required, though it’s often advisable. Premiums in Zone X are typically low, sometimes under $500 annually through the National Flood Insurance Program.

Zone AE — high-risk flood zone with an established base flood elevation. Federally-backed mortgage holders are required to carry flood insurance. NFIP premiums here vary significantly by elevation relative to the base flood elevation — properties that sit well above the BFE on a flood elevation certificate may qualify for substantially lower rates.

Zone VE — coastal high-hazard area subject to wave action in addition to flooding. These designations appear along ocean-facing beaches and certain Sound-facing bluffs. VE zone insurance is typically the most expensive, because the actuarial risk is highest.

Zone AO — shallow flooding areas, often near overland flow paths. Common in older suburban areas where storm drainage infrastructure is strained.

When a property moves from Zone X to Zone AE or VE through a FIRM update, a homeowner with a federally-backed mortgage may receive notification from their lender that flood insurance is now mandatory. If they purchase an NFIP policy at standard rates without a flood elevation certificate documenting their actual structural elevation, they may pay far more than necessary. A licensed surveyor’s flood elevation certificate — which documents the finished floor elevation of the structure relative to the base flood elevation — can dramatically reduce the policy premium.

The reverse also happens: properties that move out of mandatory zones through a map update or a successful LOMA appeal may find their lender’s requirement lifted, reducing their monthly cost of ownership.

Steps to Take If Your Property Just Entered a High-Risk Zone

The process is not automatic, and homeowners who wait for their lender or insurance company to manage this for them often pay more than they need to.

First: pull the current FIRM at msc.fema.gov. Identify your flood zone, the effective date of the map panel, and whether any Letter of Map Change is pending for your community. Suffolk County’s floodplain administrator can also confirm whether a map revision process is active in your area.

Second: commission a flood elevation certificate from a licensed surveyor or engineer. This document takes the actual elevation of your lowest floor, the ground beneath your structure, and any attached garage and compares them to the base flood elevation shown on the map. If your structure sits above the BFE — which many older North Shore homes built on slightly elevated lots do — the certificate is your best tool for negotiating a lower NFIP premium.

Third: contact your insurance agent with the certificate in hand before accepting any quoted premium. NFIP rates are federally set, but the rating factors they apply depend on the elevation data used, and that data has to come from somewhere. Without a current elevation certificate, the rating defaults to assumptions that often overstate risk.

Fourth: if you believe your property has been incorrectly placed in a high-risk zone — because of topography, drainage improvements, or updated hydrological data — a licensed engineer can help you prepare a Letter of Map Amendment application to FEMA requesting removal from the mandatory zone. LOMA approvals are not guaranteed, but they are obtained regularly by properties that can demonstrate their ground elevation exceeds the base flood elevation.

What Sellers Must Disclose Under New Flood Map Designations

In New York State, sellers of residential property are required to complete a Property Condition Disclosure Statement. The form asks directly about flood zone status and prior flood damage. Misrepresentation on this form carries legal liability.

Beyond the disclosure form, a buyer’s lender will run its own flood zone determination as part of the mortgage underwriting process. If the current FIRM shows the property in a high-risk zone, the lender will require flood insurance as a condition of the loan — typically before closing. This is not something that can be quietly worked around or disclosed only at the table.

For sellers, the strategic implication is this: if you are listed in a high-risk zone and hold a current flood elevation certificate showing your structure sits above the base flood elevation, include that document in the listing file and share it with buyers early. A certificate that translates to a $400 annual NFIP policy rather than a $4,000 one changes the buyer’s cost calculus materially. That’s a selling asset.

If you don’t have a current elevation certificate and your property carries a Zone AE or VE designation, I’d recommend getting one before listing. The cost is typically $400 to $700. The impact on your buyer pool — and on price negotiations — is often worth multiples of that.

How to Appeal a FEMA Flood Zone Classification

FEMA’s map amendment and revision process exists precisely because maps are imperfect representations of complex terrain, and individual properties sometimes land in zones that don’t accurately reflect their actual flood risk.

A Letter of Map Amendment (LOMA) is the appropriate tool when an individual property or structure has been inadvertently included in a Special Flood Hazard Area because its natural ground elevation is at or above the base flood elevation. A licensed land surveyor or engineer prepares the documentation — primarily an elevation certificate — and submits it to FEMA. FEMA reviews the data and, if the evidence supports it, removes the property from the mandatory purchase requirement.

A Letter of Map Revision (LOMR) addresses larger-scale situations — a new detention basin, a stream channel modification, or significant fill operations that have altered the hydrological conditions underlying the map.

Both processes take time — typically 60 to 90 days for a LOMA, longer for a LOMR. For a transaction with a defined timeline, the buyer’s and seller’s attorneys need to understand what happens if the determination doesn’t arrive before closing. There are workarounds — FEMA’s Provisional Acceptance of a LOMA (PAL) process allows lenders to treat a pending application as conditionally approved — but these require coordination.

I always recommend that buyers of waterfront or near-waterfront properties in Suffolk County engage their own flood zone consultant or surveyor independent of the seller’s disclosure. The stakes are too high — both in insurance cost and in post-Sandy understanding of what high-risk designation actually means for a property — to rely solely on representations made at the time of listing.

Real estate markets change. This post reflects conditions as of May 2026. For current listings and market data, contact Pawli at Maison Pawli.

This is for informational purposes only — consult a licensed attorney, financial advisor, or licensed surveyor for your specific situation. Flood zone determinations and insurance requirements vary by property.

Sources

– FEMA Map Service Center — msc.fema.gov – FEMA Flood Maps — fema.gov – Suffolk County, NY — Am I At Risk? Flood Zone Information – PropertyShark — FEMA Flood Zone Map of Suffolk County, NY – FEMA Community Listing for New York State — floodmaps.fema.gov

You Might Also Like

– Flood Insurance on Long Island’s North Shore: What FEMA Maps Don’t Tell You About Sound-Facing Properties – Sound vs. Bay vs. Harbor: What the Water Type Actually Means for Your Maintenance Budget and Resale Value – Dock Rights, Riparian Claims, and the Fine Print: What Waterfront Buyers on Long Island Sound Actually Own