The Science of Why We Overpay for Houses — And How to Stop

You think you’re buying a house. You’re actually running a feelings experiment with a thirty-year mortgage attached to it. The research is not flattering.

Daniel Kahneman spent a career documenting the gap between how humans believe they make decisions and how they actually make them. The gap is enormous. It does not close just because the stakes are high. In fact — and this is the finding that should keep every homebuyer up at night — high stakes often make the cognitive distortions worse. The brain under pressure is not a more accurate instrument. It’s a faster one. Fast in the wrong direction.

Real estate is a perfect laboratory for this. You’ve got massive financial stakes. You’ve got artificial scarcity (“there are two other offers”). You’ve got time pressure (“we need a decision by 5pm”). You’ve got aesthetic manipulation — the fresh paint smell, the staged throw pillows, the music they play at open houses that you don’t consciously notice but that absolutely affects how you feel in the space. And underneath all of that, you’ve got a brain running software that evolved to make fast tribal decisions on the African savanna, now asked to evaluate comparable sales data in Suffolk County.

The researchers who have studied this don’t find it surprising that buyers overpay. They find it surprising that buyers don’t overpay more.

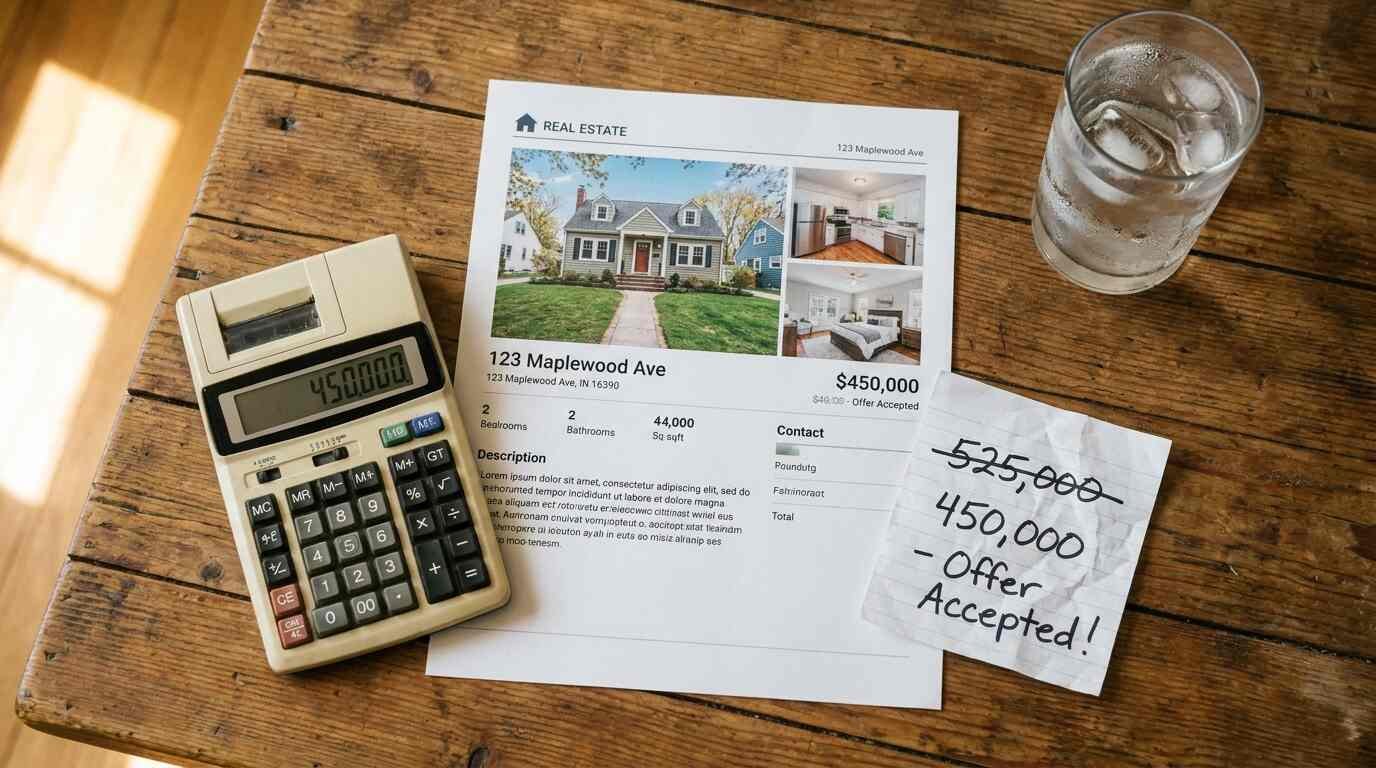

Anchoring Bias: Why the List Price Is a Trap

Kahneman and Tversky’s 1974 paper on heuristics and biases introduced the world to anchoring — one of the most robust findings in all of cognitive psychology. The mechanism is simple. When people make estimates under uncertainty, they latch onto a reference number — any reference number, even a random one — and adjust from it insufficiently. The anchor shapes the final estimate far more than it should.

List price is an anchor. A powerful one. The seller and their agent chose it strategically. It may or may not bear any relationship to what the property is actually worth. It may be set high to allow room for negotiation. It may be set low to create a bidding war. Either way, it is not a neutral piece of information, and the moment you register it, it has begun to influence your valuation.

The behavioral science blog Absolute Decisions put the real estate version of this well: the anchoring effect means it is “simply easier to accept the anchor (e.g., the house seller’s asking price) and adjust closely to the anchor (e.g., £50,000 less rather than £150,000) than to make an entirely new judgement about something (e.g., the value of the house).” That’s the trap in three sentences. The adjustment isn’t random — it’s systematically biased toward the number they gave you first.

The research on real estate specifically — and this has been studied directly, not just extrapolated from laboratory conditions — shows that buyers exposed to higher list prices consistently offer more for identical properties than buyers exposed to lower list prices. Not slightly more. Meaningfully more. The anchor effect survives even when buyers know they should be skeptical of the list price.

The counter-strategy isn’t complicated, but it requires discipline. Before you see any list price, build your own value estimate. Look at the comparable sales — actual closed transactions, not asking prices, not Zestimate approximations, but what properties have sold for in that neighborhood in the past ninety days. Write down a number. Then look at the list price. The gap between your number and the list price is information. Which way does the gap cut? That question is more useful than anything the listing agent will tell you.

The Endowment Effect and Why Sellers Always Think Their House Is Worth More

Richard Thaler — Nobel laureate in economics, 2017 — built much of his career on the endowment effect: the documented tendency for people to overvalue things they own relative to identical things they don’t. Once something is yours, losing it feels worse than an equivalent gain would feel good. Loss aversion is asymmetric. Ownership creates attachment that distorts price.

For sellers, this is almost universal. They have lived in the house. They have memories in it. They paid for the kitchen renovation. They know which neighbor has the good dog and which one plays music too loud on Saturdays. None of that transfers to the buyer. None of it is worth anything in the comparable sales analysis. But it inflates the seller’s internal sense of what the house is worth, sometimes by a lot.

Genesove and Mayer documented this rigorously in a 2001 paper in the Quarterly Journal of Economics, looking at Boston condo sellers who were facing nominal losses — sellers who had paid more for the property than they could currently sell it for. Those sellers listed at higher prices, took longer to sell, and ultimately received higher prices than loss-neutral sellers — but they also had dramatically longer days on market and a meaningfully lower sale rate. The loss aversion was costing them time and probability of sale in exchange for a small average price bump. That’s not a winning trade. But the brain doesn’t process it that way. The brain is defending against loss, not optimizing for outcome.

For buyers, the endowment effect operates on the other side of the transaction: the fear of not getting the house. Once you’ve mentally placed yourself in the house, you’ve effectively begun to feel ownership of it. The prospect of losing it activates the same loss-aversion circuitry. That’s when the brain starts finding reasons to justify overpaying — “it’s a hot market,” “we’ll make it up,” “this one is special” — and stops running the numbers.

You know you’ve hit this point when you start arguing against yourself. When the voice that says “the inspection was rough, we should renegotiate” is getting drowned out by the voice that says “but we love this house.” That second voice is not giving you information about the house. It’s giving you information about your attachment to it.

FOMO Bidding Wars: What the Research Says About Auction Fever

The behavioral economics literature calls it auction fever. The mechanism is well-documented. In competitive bidding situations, the act of competing changes the way people value the object being bid on. Winning becomes a goal in itself. The price you’re willing to pay drifts upward not because your assessment of value has changed but because you don’t want to lose.

This has been studied in actual real estate markets. Research published in the Journal of Real Estate Finance and Economics has documented systematic patterns of overbidding in competitive housing markets — where the winning bid in multiple-offer situations consistently exceeds what subsequent resale data suggests the property was worth. The winner wins the house and overpays for it. The phenomenon has a name in the academic literature: winner’s curse.

The multiple-offer scenario that real estate agents present as exciting — “there are three other offers, you’ll need to go best and final” — is, from a behavioral economics standpoint, precisely the conditions designed to maximize irrational bidding. Time pressure. Competition. Artificial scarcity. Emotional investment. The brain under those conditions is not the brain you want making a six-figure financial decision.

The hard part is that you can know all of this and still be susceptible to it. Knowing about the anchor doesn’t eliminate anchoring. Knowing about auction fever doesn’t make you immune to it. What it does is give you a framework to build guardrails before you’re in the room.

The guardrail that actually works: set your maximum before you make any offer, based on your own comparative analysis and your own financial situation, and treat that number as fixed. Not as a starting point. Fixed. Write it down. Share it with your spouse or partner if you have one. Tell your agent. Make it external and accountable. The brain will try to renegotiate it in the moment. Your job is to not let it.

How to Build a Decision Framework That Overrides Your Own Brain

The research on debiasing — on how to actually counteract cognitive biases rather than just knowing about them — is more mixed than the research on the biases themselves. Simply knowing you’re susceptible to anchoring doesn’t reliably reduce anchoring. What helps is procedural. Pre-commitment. External structure. Slowing down.

For real estate specifically, here is what the behavioral literature supports:

Do the comparables analysis before seeing the property. Not after. Before. Your valuation should be formed from data before it has a chance to be contaminated by how the afternoon light hits the living room.

Separate the decision from the urgency. The “offer by 5pm” deadline is almost always artificial. Not always, but almost. Slow down where you can. The properties that “have to be decided on tonight” and then close immediately are rarer than the pressure implies.

Use a checklist for the inspection. Not notes. A checklist. The inspection report surfaces findings in a specific order that may not reflect their financial importance. A categorized checklist — mechanicals, structure, water, environmental — forces systematic evaluation rather than emotional triage.

Model the cost of being wrong in both directions. If you overpay by $30,000, what does that actually cost you over a 30-year mortgage? Calculate it. It’s a real number, and it’s usually smaller than the emotional weight it carries. Conversely, if you lose the house by $10,000, you lose a house. There will be other houses. The market does not offer single unique opportunities as often as the psychology of any specific transaction makes it feel.

None of this is cold or unemotional. Buying a house is one of the most significant decisions most people make. It should carry weight. The weight is appropriate. The distortion is not.

What a Good Agent Does — and What Your Gut Does — When They Conflict

Here’s where the rubber meets the road. You’ve done your comparables. You’ve set your number. You like the house. Your agent tells you the comparables don’t support going above $X. Your gut says go to $X plus $40,000 because you want this house and you’re afraid of losing it.

A good agent is giving you information. Your gut is giving you feelings. Both are inputs. The question is which one has more relevant signal for the decision at hand.

What a good buyer’s agent actually does — a function that gets undersold in every conversation about real estate commissions — is serve as a behavioral circuit breaker. They have seen this particular movie many times. They know when a market is genuinely competitive and when urgency is being manufactured. They know when a list price reflects actual value and when it’s a trap. They have no attachment to the house. They are running the transaction, not falling in love with the kitchen.

That distance is worth something. Sometimes it’s worth the gap between the price your gut wanted to pay and the price the numbers support.

What your gut is good at: red flags. The house that doesn’t feel right for reasons you can’t fully articulate but are usually pointing at something real — the layout that doesn’t work for your actual life, the neighborhood that doesn’t match the photos, the seller who is evasive in ways that make you want to read the disclosure form more carefully.

Use your gut for red flags. Use the research for prices.

The behavioral economics literature doesn’t say emotions are bad inputs into real estate decisions. It says they’re bad inputs into pricing decisions. The two things are not the same. Whether to want a house is partly emotional and appropriately so. What to pay for it is a calculation, and the calculation should be done by the part of your brain that doesn’t care whether you love the backyard.

Those two things — the wanting and the pricing — are easier to separate when someone walks you through it. The best agents I’ve seen on the North Shore do exactly that. They let you fall in love with the property. And they keep you honest about the number.

The research is on your side. Use it.

You Might Also Like

- The Buyer Who Walked Through an Open House Twice and Paid $40,000 Less

- How to Choose the Right Real Estate Agent on Long Island

- Days on Market Is a Calculated Figure, Not a Raw Fact

This post is for informational purposes only and does not constitute financial or legal advice. Consult a licensed real estate attorney and financial advisor for guidance specific to your situation.

Real estate markets change. For current listings and market data, contact Pawli at Maison Pawli.

Sources

- Kahneman, D. & Tversky, A. (1974). “Judgment under Uncertainty: Heuristics and Biases.” Science, 185(4157), 1124–1131. https://www.science.org/doi/10.1126/science.185.4157.1124

- Thaler, R. (1980). “Toward a Positive Theory of Consumer Choice.” Journal of Economic Behavior and Organization, 1(1), 39–60.

- Genesove, D. & Mayer, C. (2001). “Loss Aversion and Seller Behavior: Evidence from the Housing Market.” Quarterly Journal of Economics, 116(4), 1233–1260. https://doi.org/10.1162/003355301753265561

- Ku, G., Malhotra, D., & Murnighan, J.K. (2005). “Towards a Competitive Arousal Model of Decision-Making.” Organizational Behavior and Human Decision Processes, 96(2), 89–103.

- Kahneman, D. (2011). Thinking, Fast and Slow. Farrar, Straus and Giroux.

- Absolute Decisions Blog. “The anchoring and adjustment heuristic in real estate transactions.” https://absolutedecisionsblog.wordpress.com/2016/12/31/the-anchoring-and-adjustment-heuristic-in-real-estate-transactions/