The Mortgage Commitment Letter Is Not a Loan Approval: The Legal Distinction That Collapses Transactions at Closing

Sellers who accept an offer on the basis of a mortgage commitment letter believe they have evidence of financing. They are correct — but only in a conditional sense that most sellers do not examine carefully enough, and that some buyers understand even less well than their sellers do.

The commitment letter is the document that separates the pre-qualification stage from the contract stage in most residential transactions. It is presented as proof that the buyer can buy. What it actually is — with precision — is a conditional promise to lend, subject to a list of conditions that may or may not have been satisfied by the time the letter was issued, and that remain outstanding in ways that can unravel the transaction entirely.

The Regulatory Framework

TRID — the TILA-RESPA Integrated Disclosure Rule, 12 C.F.R. § 1026.19 — governs what lenders must disclose to borrowers and when. The Loan Estimate, provided within three business days of loan application, sets the terms the lender intends to offer. The Closing Disclosure, provided three business days before consummation, reflects the final loan terms.

Neither the Loan Estimate nor the Closing Disclosure is the commitment letter. The commitment letter is an informal document — not regulated by TRID, not defined by Regulation Z in any binding way — that a lender issues to communicate to the borrower and, typically, to the seller and their agent, that the loan has been conditionally approved.

Regulation Z, 12 C.F.R. § 1026.2(a)(13), defines “consummation” as the moment the borrower becomes contractually obligated on the loan — which in most states means the moment documents are signed at closing. Consummation is not commitment. A mortgage commitment letter does not obligate the lender to fund. It obligates the lender to proceed toward funding — subject to the conditions it contains.

Conditions Precedent: What They Are and Why They Matter

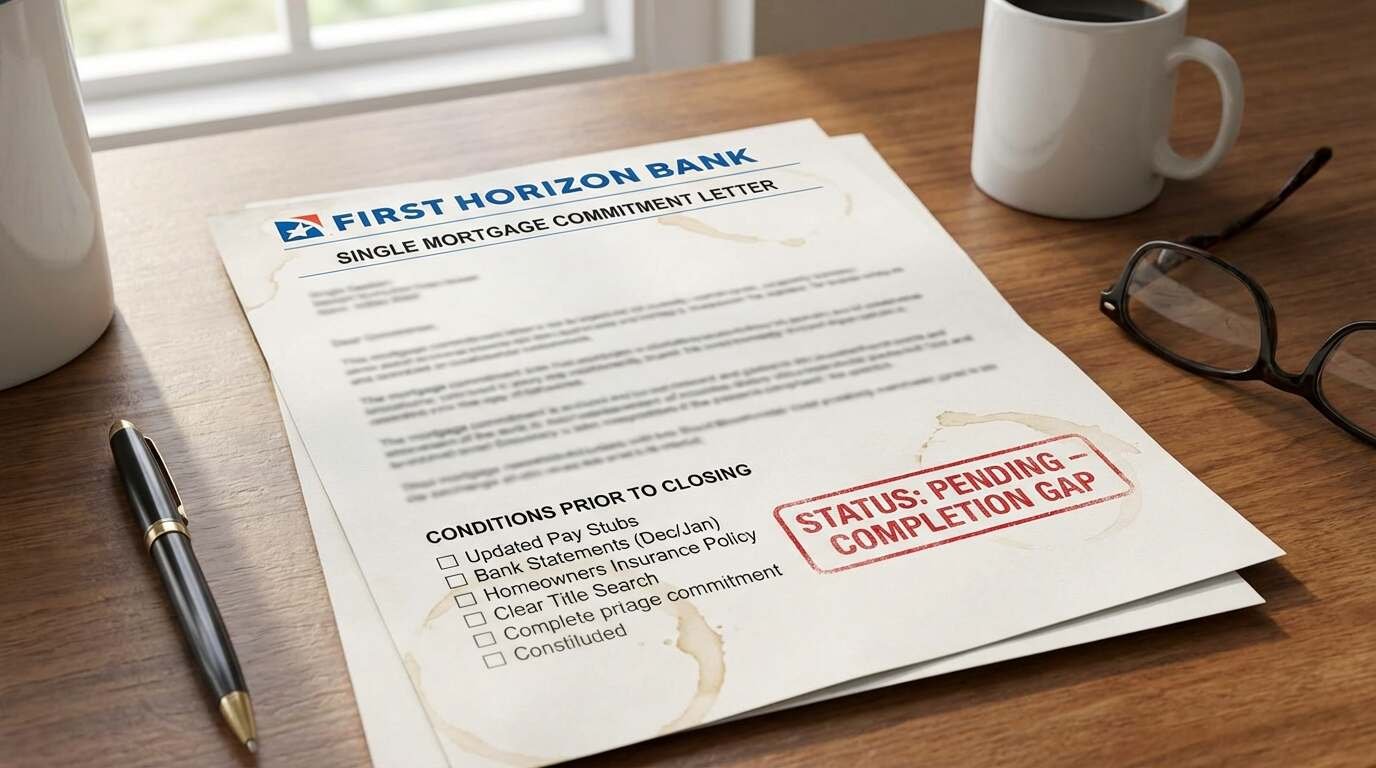

Every mortgage commitment letter contains conditions. Some are standard and mechanical: satisfactory appraisal, title insurance commitment, flood zone certification, hazard insurance binder. Others are borrower-specific: updated pay stubs through a certain date, a letter of explanation for a credit inquiry, verification of a gift fund, resolution of a tax lien that appeared in the credit pull.

Fannie Mae’s Selling Guide, B3-2-10, addresses underwriting conditions in detail. The distinction the Guide draws — and that the commitment letter embodies — is between conditions that have been satisfied as of the date of issuance and conditions that remain outstanding. A commitment letter that issues with outstanding conditions is not a loan approval. It is a roadmap to approval, with the conditions as the route.

The conditions that generate late-stage transaction failures are typically the ones that were incomplete at the time of commitment: the appraisal hasn’t been ordered yet, the borrower’s employment needs verification, the flood zone designation requires a letter of map amendment. When these conditions can’t be satisfied — or can’t be satisfied in time — the financing contingency is triggered, and the transaction either extends or collapses.

What the Financing Contingency Protects — and What It Doesn’t

A well-drafted financing contingency protects the buyer’s earnest money if the buyer cannot obtain the specified loan on the specified terms by the specified date. It is, in that sense, the buyer’s principal protection against the gap between the commitment letter’s conditional promise and the lender’s actual funding.

The protection is not unlimited. A financing contingency that has been removed — either actively, in a California-style removal jurisdiction, or passively, in a jurisdiction where the deadline’s expiration constitutes waiver — does not protect the buyer if the loan subsequently fails. A buyer who removed the financing contingency before the commitment conditions were all satisfied has accepted the risk that those conditions might not be met.

This is the scenario that generates both the litigation and the forfeited earnest money deposits that appear in financing contingency case law. The buyer’s agent communicated that “we’re good on financing” before the underwriting was actually complete. The contingency was removed. The lender subsequently identified an unresolved condition. The loan didn’t fund. And the buyer’s earnest money was at risk because the contingency was gone.

Seller Exposure in This Scenario

Sellers who accept offers and take their property off the market based on a commitment letter with outstanding conditions are also exposed — not financially, typically, but temporally. A transaction that collapses at the commitment condition stage three weeks before closing has cost the seller weeks of market time, potentially the loss of other interested buyers, and an inevitable conversation with their broker about how to represent the property’s history to the next buyer without generating DOM stigma.

The more sophisticated approach for sellers — particularly in markets where buyer financing quality varies significantly — is to ask to see the commitment letter, not just receive confirmation that one has been issued. The conditions page of the commitment letter tells you more about the actual financing status than the cover page does.

What Buyers Should Do

Before removing any financing contingency, buyers should request confirmation from their lender that all conditions in the commitment letter have been satisfied — not that they expect to satisfy them, but that they have. This confirmation should be in writing. Lenders who say “we’re in great shape” without documenting cleared conditions are offering assurance, not evidence.

Buyers should also understand the difference between a commitment letter and a clear-to-close — the lender’s signal that all conditions have been satisfied and the loan is ready to fund pending document signing. The clear-to-close is the practical equivalent of a funded loan for transaction purposes. The commitment letter is not.

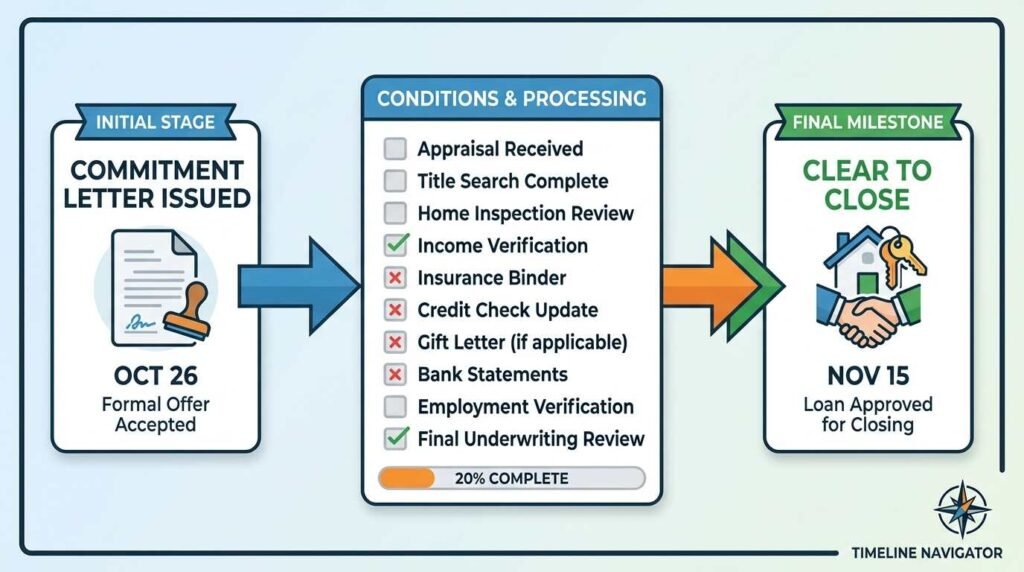

The mortgage process has a well-defined sequence: application, conditional approval, condition satisfaction, clear-to-close, closing, funding. The commitment letter belongs early in that sequence. Treating it as the end of the sequence is the error that closes transactions before they close.

This post is for informational purposes only and does not constitute legal or financial advice. Mortgage requirements vary by lender, loan type, and jurisdiction. Consult a licensed real estate attorney and mortgage professional before removing any financing contingency.

Sources:

- TILA-RESPA Integrated Disclosure Rule (TRID), 12 C.F.R. § 1026.19: https://www.consumerfinance.gov/rules-policy/final-rules/tila-respa-integrated-disclosure-rule/

- Regulation Z, 12 C.F.R. § 1026.2(a)(13): https://www.ecfr.gov/current/title-12/chapter-II/part-1026

- CFPB Loan Estimate and Closing Disclosure forms: https://www.consumerfinance.gov/owning-a-home/

- Fannie Mae Selling Guide B3-2-10: https://selling-guide.fanniemae.com

You Might Also Like: The Complete Guide to Buying a Home on Long Island’s North Shore — the full buyer’s guide covering every stage of the North Shore home purchase, from mortgage to closing.