Buying Waterfront Property on Long Island’s North Shore: What Every Buyer Needs to Know

The first time I showed a waterfront home on the North Shore, the buyer spent the entire walk-through looking at the water. He barely glanced at the kitchen. He didn’t open a single closet. When we got back to the car, he said, “I’ll take it.”

I talked him out of making an offer that day. Not because the house wasn’t beautiful — it was — but because he hadn’t asked a single question about the bulkhead, the flood zone designation, the DEC adjacent area setbacks, or whether the dock he was already mentally building would require four separate permits and eighteen months of waiting. He thanked me later. The house he eventually bought, three months down the road, came with a bulkhead that had been replaced two years prior, a survey that clearly delineated the riparian boundary, and a FEMA zone classification that kept his insurance costs manageable.

Waterfront property on Long Island’s North Shore is unlike anything else in the regional market. The emotional pull is enormous — morning light on the Sound, the smell of salt air through an open window, a private beach at the bottom of a bluff. But the regulatory, financial, and structural realities of owning property at the water’s edge are more complex than most buyers anticipate. This guide covers every dimension of that complexity, and links to the deeper reporting I’ve published on each subject over the past year.

The North Shore Waterfront Is Not One Market — It’s Several

When buyers say they want a waterfront home on the North Shore, they often haven’t yet distinguished between the fundamentally different types of waterfront they’re considering. A Sound-facing bluff property in Nissequogue operates under entirely different physical, regulatory, and insurance conditions than a harbor-front home in Port Jefferson or a creek-side parcel in Stony Brook. The water type — open Sound, protected harbor, tidal creek, freshwater pond — determines your maintenance trajectory, your insurance costs, your permit requirements, and in many cases, the long-term structural demands on the property itself.

I wrote a full breakdown of what the water type actually means for your budget and your resale position in Sound vs. Bay vs. Harbor: What the Water Type Actually Means for Your Maintenance Budget and Resale Value. If you’re early in your search, that piece will reframe how you think about your options.

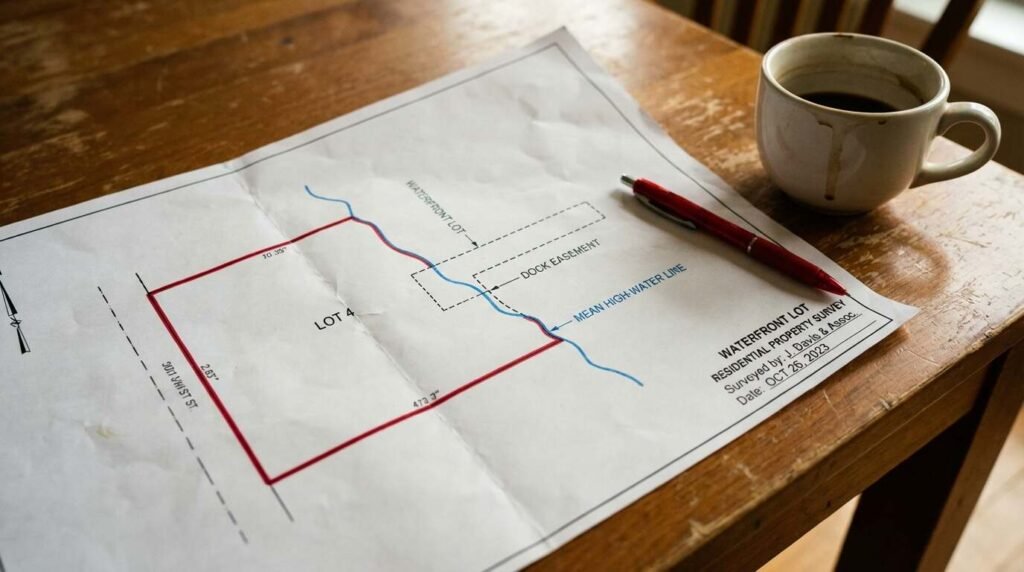

What You Actually Own When You Buy Waterfront

One of the most persistent misunderstandings in waterfront real estate is the assumption that buying a waterfront home means you own the water. You don’t. On Long Island, riparian and littoral rights grant waterfront property owners certain use privileges — access, reasonable use, the right to build a dock subject to permits — but the land beneath navigable waters belongs to the State of New York. Your property line may extend to the mean high-water mark, or it may not. It depends on the deed, the survey, and in some cases, grants and patents that predate the American Revolution.

I covered the legal complexity of where waterfront property actually ends — including dock rights, riparian boundaries, and the distinction between deeded water access and assumed water access — in Where Does Your Property Actually End? The Legal Swamp of East End Dock Rights. Any buyer considering a waterfront purchase should read it before scheduling a second showing.

Erosion Is Not a Theoretical Risk on the North Shore

The North Shore bluffs are glacial deposits — unconsolidated sand, clay, and gravel left behind by the Wisconsin Ice Sheet. They erode. Some years slowly, some years dramatically. A nor’easter can take six feet of bluff face in a single storm. Buyers who fall in love with a bluff-top view need to understand that the view may move closer to the house over time, and that the legal and engineering options for addressing bluff erosion are more limited than most people assume.

Armoring a bluff with a seawall or revetment requires DEC permits and Army Corps of Engineers review. The permitting process can take well over a year, and the regulatory preference is increasingly toward managed retreat and soft stabilization rather than hard armoring. I walked through the full picture — the science, the permitting, and the financial implications — in North Shore Bluff Homes and the Erosion Question: What Buyers Need to Know.

The Bulkhead Question

If the property sits on the harbor or along a tidal creek rather than atop a bluff, the structural question shifts from erosion to bulkheads. A bulkhead in good condition is a significant asset. A bulkhead in failing condition is a five- to six-figure liability that most buyers dramatically underestimate.

Replacement costs on the North Shore for a timber bulkhead run between $800 and $1,500 per linear foot, and that’s before the DEC permitting, the engineering survey, and the environmental compliance work. A vinyl sheet pile bulkhead costs more but lasts longer. Either way, a buyer looking at a waterfront property with an aging or compromised bulkhead needs to price that replacement into the offer — not as a future project, but as an immediate cost of acquisition.

I covered the economics, the engineering, and the permitting timeline in detail in Holding Back the Sound: The Brutal Economics of North Shore Bulkheads.

Flood Insurance: What FEMA Maps Tell You and What They Don’t

Every waterfront buyer on Long Island encounters the FEMA Flood Insurance Rate Map. What most buyers don’t understand is that FEMA maps are backward-looking documents — they reflect historical flood data and modeling, not necessarily the current or emerging risk profile of a property. FEMA’s Risk Rating 2.0 methodology, introduced in recent years, has moved toward more individualized premium calculations that factor in a property’s specific elevation, distance from water, and replacement cost. But the maps themselves still lag behind the physical reality in many North Shore communities.

A property classified in Zone X (moderate to low risk) can still flood. A property in Zone AE (high risk) may sit higher than its neighbors and face less actual exposure than the map suggests. The flood zone designation drives your insurance obligation — if you’re in a high-risk zone with a federally backed mortgage, flood insurance is mandatory — but the designation alone doesn’t tell you what your annual premium will be, what your actual exposure is, or whether private flood insurance might offer better terms than the NFIP.

I wrote a detailed guide to navigating all of this specifically for North Shore buyers in Flood Insurance on Long Island’s North Shore: What FEMA Maps Don’t Tell You About Sound-Facing Properties.

The DEC Permit That Nobody Mentions at the Showing

This is the one that catches buyers off guard more than anything else. New York State’s Department of Environmental Conservation regulates activities in tidal wetlands and their adjacent areas under the Tidal Wetlands Act. On Long Island, the adjacent area extends up to 300 feet inland from the wetland boundary. That means a renovation, an addition, a new deck, even significant landscaping work on a waterfront property can trigger a DEC permit requirement — even if the work itself is entirely upland and doesn’t touch the water.

The permit process involves application fees, environmental assessment forms, site surveys showing the tidal wetland boundary, and in many cases, a months-long review period. Failure to obtain the required permits before starting work exposes both the property owner and the contractor to DEC enforcement action. For buyers planning any kind of post-purchase renovation on a waterfront property, understanding the DEC’s jurisdiction before closing is not optional — it is a financial and legal necessity.

I published a full walkthrough of the DEC tidal wetlands permit process as it applies to Long Island waterfront homeowners in The DEC Permit Nobody Mentions at the Showing: Wetlands Regulations and Long Island Waterfront Renovation.

The Inspection Is Different on the Water

A standard home inspection covers the roof, the foundation, the electrical, the plumbing, the HVAC. On a waterfront property, that checklist is only the beginning. The inspection needs to include the condition of the bulkhead or seawall, the state of any docks or pilings, evidence of water intrusion from storm surge (distinct from basement moisture), salt air corrosion on exterior systems, and — critically — the condition of the septic system relative to the water table and the tidal wetland setback requirements.

I always recommend that waterfront buyers hire a marine contractor or structural engineer to inspect the bulkhead and any waterside structures separately from the general home inspection. The general inspector is looking at the house. The marine specialist is looking at the interface between the house and the water — and that interface is where the most expensive surprises hide.

The Eelgrass Problem and Environmental Health

Not every waterfront concern is structural or regulatory. On the East End and increasingly along parts of the North Shore, the ecological health of the water itself has become a material factor in property value. The collapse of eelgrass beds in Peconic Bay — driven by nitrogen loading from septic systems, fertilizer runoff, and climate-related water temperature increases — has degraded water quality, reduced shellfish populations, and raised questions about the long-term environmental sustainability of bayfront living.

Buyers considering bayfront property anywhere on Long Island should review the water quality monitoring data for the specific embayment or harbor. I reported on the eelgrass crisis and its implications for bayfront buyers in The Eelgrass Crisis in Peconic Bay — and Why Every Bayfront Buyer in Southold and Shelter Island Should Read the Water Quality Data Before Closing.

Estate Conversions: The Carriage House Premium

One of the more surprising dynamics in the North Shore waterfront market is the emergence of converted outbuildings — carriage houses, gate lodges, gardener’s cottages — as premium properties in their own right. Many of these structures sit on waterfront or water-adjacent parcels that were subdivided from larger Gold Coast estates during the mid-twentieth century. The conversions often retain architectural character that new construction can’t replicate, and the lots they sit on frequently include mature landscaping, established drainage, and — in some cases — deeded water access that predates modern zoning.

I covered this dynamic and its pricing implications in What the Carriage House Knows: How Long Island’s Converted Outbuildings Are Commanding Prices That Challenge the Main House.

Before You Make an Offer: The Waterfront Buyer’s Checklist

Every waterfront property I show, I walk buyers through the same set of questions before we get to the offer stage. These aren’t optional. They’re the minimum diligence required to make an informed decision on a property where the water is as much a part of the purchase as the house.

The questions that matter:

- What is the FEMA flood zone designation, and what will flood insurance cost annually under current Risk Rating 2.0 pricing?

- Is the property within 300 feet of a DEC-mapped tidal wetland, and what does that mean for planned renovations?

- What is the condition, age, and material of the bulkhead, and what is the estimated replacement cost?

- Does the survey clearly delineate the property boundary relative to the mean high-water mark?

- What are the riparian or littoral rights associated with the property, and are they deeded or assumed?

- Is there an existing dock, and is it permitted? If there is no dock, can one be permitted under current regulations?

- What is the septic system’s proximity to the tidal wetland boundary, and does it meet current DEC setback requirements?

- Has the property flooded in the last twenty years, and if so, were repairs made to code?

- What is the bluff recession rate (if applicable), and has any stabilization work been done?

These questions don’t make the purchase less exciting. They make the purchase smarter. And on the North Shore, where the right waterfront property holds its value across generations, smart is the only way to buy.

Start With What You Know

If you’re beginning a waterfront search on Long Island’s North Shore, the best thing you can do is educate yourself before you fall in love with a view. The linked posts throughout this guide go deep on every dimension of waterfront ownership — from the financial to the structural to the regulatory. Read them. Bring questions. And when you’re ready to look at properties, bring a broker who knows what to look for beneath the surface.

Real estate markets change. This guide reflects conditions and regulatory frameworks as of April 2026. For current listings and market data, contact Pawli at Maison Pawli.

You Might Also Like

- North Shore Bluff Homes and the Erosion Question

- Holding Back the Sound: The Brutal Economics of North Shore Bulkheads

- Where Does Your Property Actually End?

- Flood Insurance on Long Island’s North Shore

- Sound vs. Bay vs. Harbor

- The DEC Permit Nobody Mentions at the Showing

- The Eelgrass Crisis in Peconic Bay

- What the Carriage House Knows

Go Deeper

These posts go further on specific topics covered in this guide.

- Dock Rights, Mooring Rights, and the Difference: What North Shore Waterfront Buyers Need to Settle Before Closing

- How to Read a Waterfront Lot Survey Before You Make an Offer