The ‘Sweat Equity Ceiling’: Why Some North Shore Fixer-Uppers Will Never Appraise Out — No Matter How Good the Renovation

There’s a house in Centerport I think about sometimes. The renovation was meticulous — new kitchen, new baths, a primary suite addition with cathedral ceilings and white oak floors. The kind of work that makes you stop in the doorway. The kind of work that took eighteen months and a contractor who cared.

The appraisal came back $180,000 below the owner’s all-in cost. Not because the work was shoddy. Not because the appraiser missed anything. The problem was the street.

This is the part of the fixer-upper calculus that nobody puts in the brochure.

What the Comps Actually Control

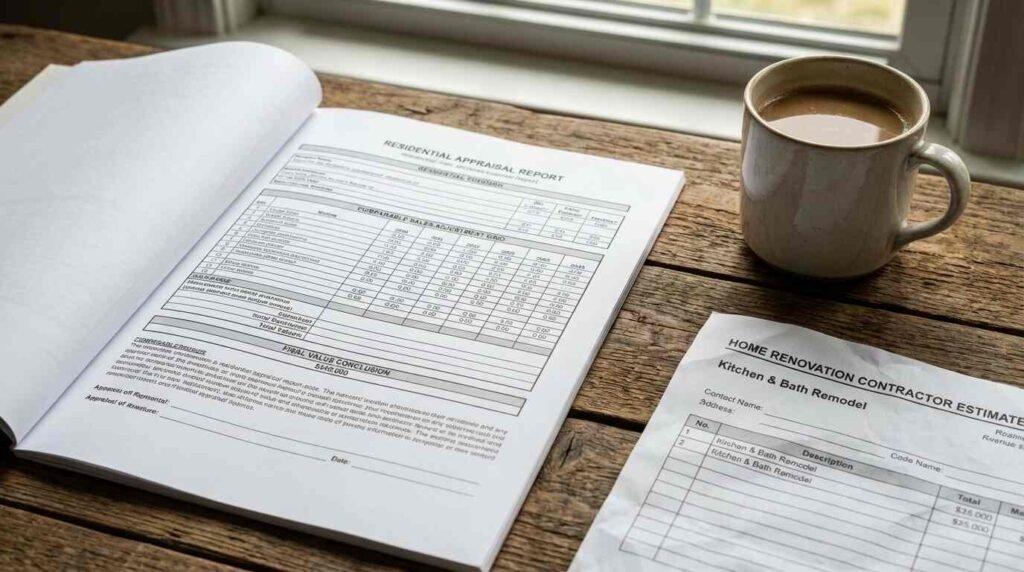

Appraisers working on conforming loans — the majority of residential transactions — operate under Fannie Mae guidelines and are bound by the Uniform Standards of Professional Appraisal Practice (USPAP). One of USPAP’s foundational principles is the concept of conformity: a property’s value is substantially determined by what similar properties on the same street, in the same school district, in the same condition have actually sold for. Appraisers don’t invent value. They discover it, and they discover it through recent comparable sales.

This is how a beautifully renovated home on a street with limited comp support ends up appraising for less than its renovation cost. The appraiser isn’t wrong. The market just hasn’t caught up — and in some locations, it may never catch up.

The renovation added genuine value. It just added it past the ceiling.

Where the Ceiling Is Lowest on the North Shore

The appraisal gap problem isn’t uniform. It’s deeply geographic, and on the North Shore it breaks along recognizable lines.

Huntington Village has long been among the most favorable zip codes for renovation ROI on the Island. The walkable downtown, the LIRR service, the concentration of buyers who want turnkey — comparable sales run high enough that quality renovations regularly support their costs. Lloyd Harbor tells a similar story: estate-scale lots, consistently strong comparable sales, buyers arriving already priced-in. Renovation investment in these markets has a reasonable chance of appraising out.

Then there are the transitional streets — and this is where buyers need to pay attention. Parts of the Centerport-to-Greenlawn corridor, pockets adjacent to Brentwood, stretches of the mid-county zip codes where the housing stock is dense and the comparable sales window is narrow. When there aren’t enough recent sales of renovated properties to anchor the appraisal, the comp pool defaults to whatever sold nearby, renovated or not. A $700,000 all-in cost on a house surrounded by $450,000 comparable sales is a math problem with no solution that a contractor can fix.

School district lines compound this. Two properties a quarter-mile apart — one inside a sought-after district, one outside it — can carry dramatically different appraisal ceilings. This is tracked in Long Island Board of Realtors (LIBOR) market data, which tracks price per square foot variations across district boundaries. The line is invisible until it shows up in a comp table.

Note: Specific zip code ROI spread data should be verified against current LIBOR market reports before publication.

How Appraisers Navigate Comp-Limited Neighborhoods

When an appraiser working in a transitional area can’t find clean comparable sales, they have a few tools — none of them perfect. They may pull comps from an adjacent neighborhood, making adjustments for location and condition. They may use older sales with time adjustments. They may assign dollar-per-square-foot values to specific improvements — new kitchen, new bath, new roof — using industry adjustment tables.

That last method is where the gap most often appears. Industry adjustment tables for kitchen renovations typically value them at a fraction of their actual cost. A $90,000 kitchen renovation might yield a $15,000–$25,000 appraisal adjustment, depending on the comp pool and the neighborhood’s price range. The adjustment reflects what the market has demonstrated it will pay, not what the improvement cost to build.

Buyers sometimes ask me why the appraiser “missed” the renovation. In most cases, they didn’t. The appraiser saw everything. The market ceiling was already set before the first permit was pulled.

The Due Diligence That Matters Before You Buy

For anyone considering a fixer-upper on the North Shore — particularly in a transitional corridor — this is the sequence that actually matters:

Request recent comparable sales before you make an offer. Not Zestimates. Not asking prices. Actual recorded sales of renovated properties within a half-mile in the past eighteen months. Your agent can pull these. If they don’t exist, that tells you something.

Know your school district line. Suffolk County Real Property Tax Service records and Nassau County Assessment Review Commission public data both allow parcel-level lookups. Verify which district you’re actually in — not which district the street feels like it’s in.

Factor in the FHA appraisal layer if applicable. As I covered in an earlier piece on the Ghost Appraiser Problem, FHA appraisals carry their own overlay of guidelines that can further compress value in markets where properties have deferred maintenance histories. If you’re using FHA financing on a fixer-upper, understand that the appraisal process will be more conservative, not less.

Talk to a local appraiser before you renovate, not after. This is advice that almost nobody takes and almost everyone wishes they had. A licensed appraiser familiar with the specific market can tell you — before you spend a dollar — what the realistic post-renovation ceiling looks like based on actual comp data. This is not the same as asking your contractor, who has every incentive to be optimistic.

Assess the street trajectory. Is this a block where prices have been moving? Is there evidence of investment — new roofs, updated siding, recent sales at the higher end of the range? Or is this a block where the most recent comps are the same houses they’ve always been? A block in early-stage transition can be a buy. A block that’s been “transitioning” for fifteen years without moving is telling you something.

The Assessed Value Problem Underneath

There’s an additional layer that trips up buyers who don’t know Long Island’s assessment structure. Suffolk County’s assessed values are frequently misaligned with actual market values — sometimes dramatically so. As I covered in the piece on Long Island’s property tax grievance process, the assessed value on a property tells you almost nothing reliable about what it will appraise for post-renovation. Buyers sometimes conflate these numbers. They’re different documents, different methodologies, and they’re used for different things.

What this means practically: a dramatically low assessed value on a fixer-upper isn’t necessarily a signal that the market has priced the property wrong. It may simply reflect Suffolk County’s rolling assessment lag, which can run years behind actual market movement.

What This Means for the Budget

The clearest way to frame the sweat equity ceiling for a buyer is this: renovation budget and purchase price must be evaluated together against realistic post-renovation comparable sales, not against the renovation’s cost. The renovation doesn’t set the value. The market does.

This sounds obvious. It is obvious. And every year, buyers on the North Shore — intelligent, research-minded people — skip this step because the house is beautiful, the vision is clear, and the contractor is confident. The appraisal is where confidence meets the market.

For a deeper look at what Depression-era construction means for the fixer-uppers you’re likely to encounter on the North Shore, the piece on pre-war FHA homes and structural quality is worth reading before you schedule an inspection.

The house in Centerport sold eventually, at a number that left the owner holding a significant loss. The renovation was beautiful. The street never caught up. Those two facts aren’t contradictions. They’re just how appraisal works — and why the first question about a fixer-upper should never be how much will the renovation cost but what will the house be worth when it’s done.

This is for informational purposes only — consult a licensed appraiser, attorney, or financial advisor for your specific situation. Real estate markets change. For current listings and market data, contact Pawli at Maison Pawli.

You Might Also Like

- The Asbestos Ceiling Nobody’s Talking About: Why Suffolk County Fixer-Uppers Are Sitting on a Hidden Renovation Budget Line

- Inside the Long Island Split-Level: The One Floor Plan That Breaks Every Renovation Rule

- The Contractor Shortage Nobody Warned You About