Down Payment Mirages: The Long Island Housing Assistance Programs That Expired Midstream — and the Buyers Left Holding the Gap

The phone call nobody wants to receive in a real estate transaction comes at different moments for different buyers. For some it’s an inspection surprise. For others it’s a financing contingency that doesn’t clear. But there is a particular kind of call — one I’ve heard about often enough over the years to treat it as a category rather than an accident — that goes something like this: a buyer has been pre-approved, has a signed contract, has a rate lock, has done the counseling, has submitted all the paperwork, and is waiting for confirmation that the down payment assistance grant they were approved for is ready to fund. And the call they get instead is that the program ran out of money before their closing date.

I want to talk about how that happens, because it is not random, and understanding the mechanics is the first step toward protecting yourself against them.

The Program That Exists and What It Actually Offers

The Suffolk County HOME Consortium Down Payment Assistance Program is a real program funded through the federal HOME Investment Partnerships Program, administered locally by Suffolk County’s Office of Community Development. In its current form, it offers eligible first-time homebuyers up to $30,000 — structured as a zero-interest deferred loan forgiven after ten years — to assist with down payment costs on a primary residence. The income threshold is 80 percent of HUD’s area median income for Suffolk County. The property value limit has varied by year; the 2024 guidelines capped eligible homes at acquisition values consistent with local affordability benchmarks.

Applications are accepted on a first-come, first-served basis, with submission deadlines that have typically run through March or April of each program year. Once a buyer receives a Purchaser Certificate — the conditional award letter from the Suffolk County Community Development Office — they have 90 days to secure a mortgage commitment and close. New construction gets a 300-day window. The program is administered in partnership with the Long Island Housing Partnership, which handles counseling certification requirements for applicants.

This is, on paper, a genuinely useful program for the buyers it’s designed to serve — people earning moderate incomes in one of the most expensive housing markets in the country, trying to bridge the gap between what they can save and what Long Island’s entry-level prices demand. In a market where a “starter home” in Smithtown or Miller Place routinely exceeds $450,000, $30,000 in down payment assistance is not a luxury. For many buyers, it is the difference between qualifying and not.

The Structural Problem: Limited Funding, First-Come Commitment

Here is where the mechanics get difficult. HOME Investment Partnerships Program funds flow from HUD to grantees — in this case, to the Suffolk County HOME Consortium — through a federal allocation formula that is set annually and is not adjustable by the county mid-cycle. The total amount available in any given program year is fixed before a single application is accepted. Suffolk County’s obligation, under federal HOME regulations, is to commit funds only up to the amount available — and the program’s own guidelines make this explicit in plain language: “funding is limited,” and the program operates “on a first-come, first-served basis until funding has been exhausted.”

The Purchaser Certificate, when issued, is a conditional commitment — conditional on the buyer completing the required steps within the specified timeframe and on the property passing HUD’s Housing Quality Standards inspection. It is not an unconditional guarantee that funds will be available at closing. The program guidelines are direct on this point: Suffolk County explicitly disclaims liability “to any party for the loss of a down payment or any other damages” arising from program ineligibility, failed inspections, or expired certificates.

The practical consequence of this structure is that in any given year, a program can award Purchaser Certificates to buyers in good faith — buyers who then proceed to negotiate contracts, retain attorneys, lock mortgage rates, pay inspection fees, and begin the closing process — and subsequently exhaust its available funding allocation before all those closings are completed. When that happens, the buyers with closing dates after the funding runs out find themselves without the assistance they had planned for, at a point in the transaction when unwinding is expensive and painful.

HUD’s Integrated Disbursement and Information System (IDIS) tracks HOME grant drawdowns by grantee and is publicly accessible, allowing anyone to review how Suffolk County’s HOME allocations have been committed and drawn over time. Suffolk County’s annual reports to HUD through the Consolidated Annual Performance and Evaluation Report (CAPER) system provide additional program-level documentation. These records can be requested and reviewed; they constitute the paper trail behind the program’s performance history.

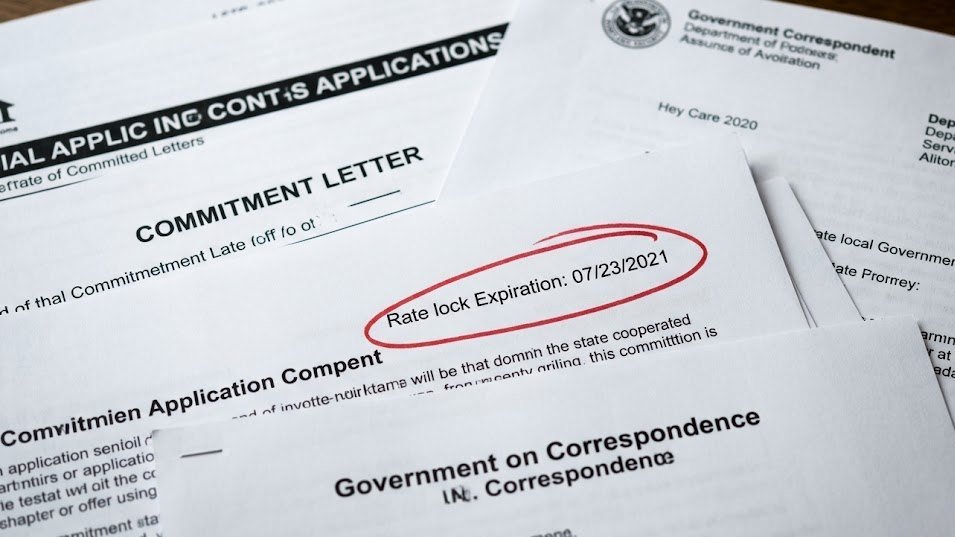

The Rate Lock Problem

When a buyer’s assistance commitment is delayed or fails to fund, the injury is not limited to the lost grant. In most mortgage transactions, the interest rate is locked for a specific period — typically 30 to 60 days from the mortgage commitment date. Rate locks expire. When they expire, the buyer must extend the lock (at a cost, often borne by the buyer) or accept whatever the current rate is on the new lock date. In a rate environment like the one that has defined the market over the past several years — volatile, often moving quickly — an expired rate lock can meaningfully change the economics of a transaction.

A buyer who structured their entire purchase around a specific rate, a specific monthly payment, and a specific down payment assistance amount may find, after a funding delay, that the transaction no longer pencils out. The rate has moved. The closing costs have increased. The assistance is uncertain. The decision they made six weeks earlier — the contract they signed, the deposit they paid, the attorney they retained — was made in a financial context that no longer exists.

Why This Happens and Why It Keeps Happening

The pattern is not the result of bad faith by the county or by HUD. It is the result of structural mismatch between the way federal housing assistance is allocated and the way real estate transactions actually work.

Federal HOME funds are appropriated annually by Congress, allocated to grantees by a formula, and must be committed and disbursed within specific federal timelines — or they face recapture. This means that grantees have an incentive to commit funds actively and early in the program year, because uncommitted funds are at risk. At the same time, real estate transactions in Long Island’s compressed market move at their own pace, shaped by inventory, negotiation, title search timelines, lender backlogs, and the Housing Quality Standards inspection schedule that HOME-funded purchases require.

The result is a timing gap. Programs commit funds based on approved applications. Closings happen when all the other transaction elements align. When the commitment period and the closing timeline don’t match — when more closings are scheduled than remaining funds can cover — some buyers lose their funding. It is a systemic problem, and it has affected buyers in Suffolk County’s program and in similar programs across Long Island during periods of high application volume.

The Specific Questions to Ask Before You Apply

None of this is an argument against applying for assistance. The Suffolk County program, when it funds, represents genuine and significant help for buyers who qualify. What it is an argument for is entering the program with clear eyes about what a Purchaser Certificate does and does not guarantee.

Before you structure your transaction around an assistance commitment, I would ask these questions directly — of the program office, of your lender, and of your attorney:

First: How much funding remains uncommitted in the current program year? The Office of Community Development can tell you this. They may not volunteer it, but they can tell you. If the program is late in its cycle and a substantial portion of funds has already been committed, your timeline risk is higher.

Second: What happens to my transaction if funding is exhausted before my closing date? Your attorney should review the program’s disclaimer language carefully and ensure your contract of sale includes a properly structured contingency that protects your deposit if the assistance fails to fund. The program’s own guidelines recommend that buyers ask their attorney to include such a clause. Make sure yours does.

Third: Can I qualify for this purchase without the assistance, and at what cost? This is not a comfortable question, but it is the essential one. If the entire transaction depends on the grant funding and there is no fallback position, the risk exposure is asymmetric. If you can qualify conventionally — even with a higher monthly payment, even without the PMI avoidance that the full down payment provides — you have options if the program funding fails. If you can’t, the risk is entirely yours to absorb.

There are alternatives worth knowing about. The Federal Home Loan Bank of New York’s Homebuyer Dream Program, available through participating member institutions including some Long Island credit unions, offers grants for down payment and closing cost assistance with broader geographic coverage and a different funding structure. CDLI (Community Development Long Island) offers low-interest second mortgage products that can function as down payment assistance without the HOME program’s first-come timing constraints. These are real options, and a good mortgage broker — or a good broker conversation before the transaction begins — can map them against your situation.

The Housing Quality Standards Inspection: Another Timing Risk

One element of the Suffolk County program that introduces its own timing uncertainty is the Housing Quality Standards inspection, which is required on all properties funded through HOME. HQS inspections are conducted by the county, not by the buyer’s private home inspector, and they have their own scheduling timelines that are not always synchronous with the buyer’s closing schedule.

A property that fails an HQS inspection — and properties can fail for conditions that a standard home inspection would note but not necessarily treat as deal-breakers — is ineligible for HOME funding until the failed items are remediated and a secondary inspection is passed. The program is explicit: it will not fund homes that fail the initial HQS inspection, and the county is not liable for deposit losses resulting from inspection failure.

This introduces a property selection consideration that most buyers don’t internalize at the offer stage: a home that is attractively priced precisely because it has deferred maintenance may be the worst possible choice for an assistance program buyer, because the very conditions that make it affordable on the surface may disqualify it from the assistance that makes it purchasable. The HQS inspection is designed to protect buyers, not to frustrate them — but its timing and outcomes need to be built into the transaction timeline from the beginning, not discovered after contracts are signed.

The Bottom Line

Down payment assistance programs in Suffolk County are real, they are federally funded, they have helped thousands of families buy homes over the years, and they are worth pursuing if you qualify. But they are not unconditional offers. They are conditional commitments made against limited annual allocations, with timing dependencies that can fail in ways that cost buyers money they cannot easily recover.

The buyers who navigate these programs successfully are the ones who went in knowing that — who structured their transaction with a contingency, who verified the funding status before committing to a timeline, who had a backup plan, and who chose a property that could pass a federal housing inspection without surprises. That is not complicated. It is just information, applied in time to be useful.

If you are a first-time buyer on the North Shore trying to figure out whether an assistance program belongs in your transaction — or which ones are worth pursuing this year — I am happy to help you think through it. Reach out through the Maison Pawli contact page. This is exactly the kind of conversation that should happen before you sign a contract, not after.

This is for informational purposes only — consult a licensed attorney or financial advisor for your specific situation.

Real estate markets change. For current listings and market data, contact Pawli at Maison Pawli.